Misconception: Bitcoin Isn't Secure & Is Too Slow

Proper comparisons invalidate misguided criticisms

If you can get over the idea of your government banning Bitcoin and realize how much value it actually has, then you might think — well how do I actually use this thing? People are accustomed to using cash, credit cards, and checks. Most never think about all that goes on behind the scenes in regards to monetary payment and settlement. Being a new technology, Bitcoin does not benefit from that same familiarity. Understandably so, people question how it works.

A couple of primary functions money serves are as a store of value and a medium of exchange:

Money as a store of value is essentially your savings. You work, earn a paycheck, use some of it, and hopefully are able to save for your future. When it comes to the money you save, you want that money to be secure from theft, loss, damage, or confiscation.

You also want your money to hold its value over time and not depreciate. Even the strongest and most stable fiat currencies in the world are continually debased, whereas Bitcoin’s programmatically enforced fixed supply addresses this issue.

Another function of money is the ability to spend it when and where you need to. If the money you had on hand was not widely accepted, that is a huge pain point — a medium of exchange should be accessible. You also want it to be fast. The last thing anybody wants is to be standing in line at Starbucks, the gas station, or the grocery store and have to wait more than few seconds for their transaction to go through.

You also want to be able to transact across space. A major problem with fiat currencies is there are so many of them, and the exchange rate between two currencies is constantly in flux. This creates a market of international exchange that consumes a lot of money but provides no real value to society. A common global money like Bitcoin can fix this.

In this article, I’m going to discuss the misconceptions that Bitcoin is too slow and that it is not secure.

Issuance, Settlements, and Payments

At its core, Bitcoin is optimized to be a currency issuer and settlement layer. I don’t want to go too deep down the ‘what is money’ rabbit hole, but the differences between the layers of our current monetary system are really important to understand before we compare Bitcoin against them.

To oversimplify things — money essentially has 3 layers: issuance, settlement, and payment. For the U.S. dollar, those layers are enacted via the Federal Reserve (issuance), commercial and retail banks (settlement), and monetary networks like Visa, Paypal, and Venmo (payment). Bitcoin can fulfill all 3 of these roles, but it is really only optimized for the first two. That’s not to say it doesn’t serve as a payments network — it certainly does — but additional layers will need to be built on top of Bitcoin in order to excel as a payments technology (similar to how additional layers are added on top of the banking system for the dollar).

I’ll touch more on payments later. For now, let’s compare Bitcoin as a currency issuer to the Fed and as a settlement layer to banks.

Currency Issuance

")

The chart above shows that the dollar has lost 90% of its purchasing power since 1950. That number is even greater (about 97%) when you date back to 1913, the year of the Federal Reserve’s creation. As the central bank of the United States, the Fed’s primary job is to issue currency.

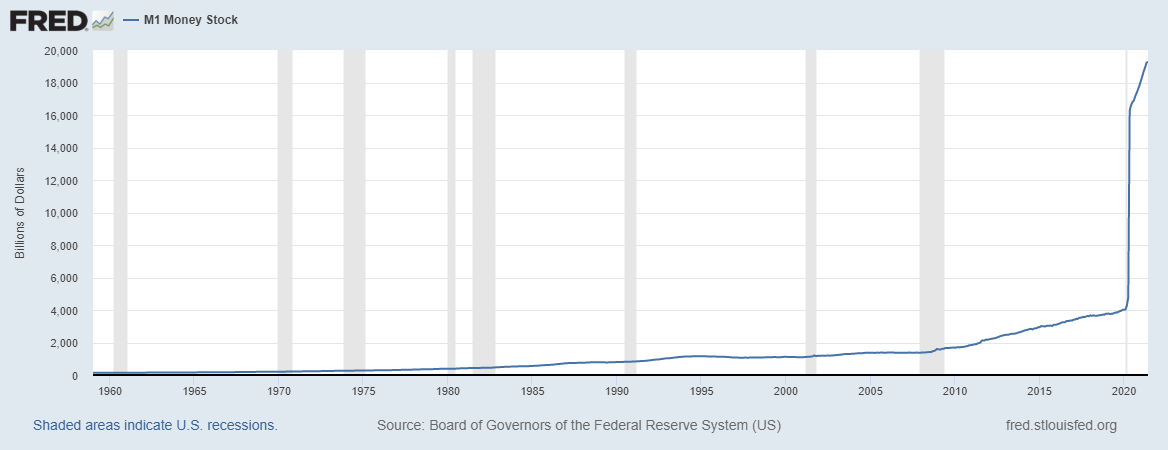

Turning our attention to the next chart, you can see a massive spike in the U.S. M1 Money Stock in 2020 and continued sharp increases throughout the first half of 2021. The M1 Money Stock represents the liquid portions of the money supply — essentially cash and cash equivalents1. At the beginning of 2020, the M1 Money Stock was about 4 trillion USD. As of June 2021, that number is creeping upwards of 20 trillion USD — nearly a 400% increase in just 18 months. No wonder CPI (Consumer Price Index, many economists’ preferred measure for inflation) recently came in higher than expected2.

So what does this all mean? And what does it have to do with Bitcoin?

This phenomenon is not unique to the United States. Central banks all over the world have progressively been printing more and more money in recent years, with no end in sight. With the creation of money, there come many promises. Some will be fulfilled, many won’t. The one thing that can be assured is that every time a central bank prints money it devalues its own citizens’ purchasing power. For the central bank of the United States, this impact is even more profound because the U.S. dollar is the world’s reserve currency — many countries and many people all around the world rely on its stability.

Bitcoin does not have this problem. Bitcoin has no central bankers, it has no central authority period. Bitcoin’s supply is fixed and its issuance rate is known. This means that over longer periods of time, Bitcoin will outperform other forms of money with an infinite supply and an unknown issuance rate (like the dollar). By these measures, Bitcoin as a currency issuer is far more effective than the Fed. The dollar may be more stable than Bitcoin today, but it will lose its value over time. Even if the Fed was able to maintain a 2% annual rate of inflation over the next 20 years, that would be a greater than 40% decline in the dollar’s purchasing power.

Settlements

Now that we’ve covered currency issuance, we can turn toward settlement. Retail and commercial banks essentially function as the settlement layer for the dollar. If we put aside the fact that 1.7 billion people (nearly one-third of the world’s population) globally are unbanked and focus just on transaction settlement in the United States, that simplifies the comparison. Below are some examples of settlement time by transaction type:

ACH (Automated Clearing House) payments encompass things like the direct deposits you get from your employer to moving money around from one bank account to another3. ACH transactions can take anywhere from a couple of days to a week or more to settle. I recently moved some money from one of my accounts to another — both accounts within the same bank — and it took 7 business days before I had access to those funds.

Wire transfers are another form of electronic money transfer where information is passed between two financial institutions. No money is initially sent from the sender to the receiver; the two institutions settle the transaction using their own reserve funds and then settle up later. Wire transfers can take less than 24 hours or up to a few days to clear between the sender and receiver. The transfer between the two intermediating institutions does not settle until afterward.

Credit card payments are ‘authorized’ right away. When you swipe your card at a store, you usually only have to wait a few seconds. But the payment does not actually settle (between the bank where your account is held and the merchant) for about 24 hours up to a few days.

Maybe you do or maybe you don’t have any complaints about the above types of transactions. With credit card payments especially, as long as it is authorized in a matter of seconds when you swipe it, you don’t have much reason to care about when settlement finality is reached.

So what does this all mean? And what does it have to do with Bitcoin?

The point I want to make with all of this is how existing types of transactions within the legacy financial system compare to Bitcoin. Bitcoin’s base layer should be compared on the basis of currency issuance and settlement, not payments. Therefore, comparing its base layer to something like Visa is an improper comparison.

In Bitcoin, on the base layer, transactions are settled approximately every 10 minutes, on average. This would be nearly 150x faster than a credit card payment settling after 24 hours. Comparing Bitcoin as a settlement layer to existing forms of transaction settlement, we see that Bitcoin is not too slow — it actually is a major improvement.

So Bitcoin is a more effective issuer of currency than central banks. It is a more effective settlement layer than commercial and retail banks. But these comparisons are meaningless if Bitcoin is not secure. Fortunately, Bitcoin is very secure.

Bitcoin Security

In my previous newsletter, I discussed the idea that governments can try to ban Bitcoin (as many have), but they cannot truly ban the Bitcoin network or stop its citizens from buying and holding Bitcoin. Bitcoin is resilient. It’s the most resilient and only truly decentralized monetary network to ever exist. For these reasons, it’s inherently secure. Security is part of Bitcoin’s DNA.

“The cost to solve a block represents the tangible resources it requires to write history to the bitcoin transaction ledger. As the network grows, the network becomes more fragmented, and the economic value compensated to miners in aggregate increases. From a game theory perspective, more competition and greater opportunity cost makes it harder to collude, and all network nodes validate the work performed by miners, which serves as a constant check and balance.” — Parker Lewis

Below, I’ll rehash some of the points I made in my prior newsletter and introduce some new ones that speak to why the network is so secure:

Bitcoin has no single point of failure. A global, decentralized network of nodes is infeasible to attack. As long as nodes are up and running all over the world, the network remains intact. In the words of SEC Commissioner, Hester Pierce, in order to truly ban Bitcoin — “You would have to shut down the internet.” I’d add that a wide range of competing nations would have to collaborate to shut down the internet across the globe.

There is no common point to ‘hack’ or ‘attack’ in a physical or digital way. China recently banned Bitcoin mining. As a result, many Bitcoin miners simply packed up their mining hardware and moved elsewhere.

There are no rulers, only consensus rules, and the value of the network is tied to the consensus staying on a common protocol. This is why just about every ‘altcoin’ ever to come into existence has failed. Bitcoin’s network effect is enormous and it continues to grow. There is much value to growing the strength of the Bitcoin network and staying on the existing protocol.

Bitcoin transactions can be done entirely peer-to-peer. Large institutions like exchanges and banks being pro-bitcoin will certainly speed up adoption, but even if they turn sour or regulation is unfriendly, Bitcoin moves along just fine via peer-to-peer transactions.

Bitcoin even survived a ‘civil war’ within the community where large players wanted to increase the block size (an effort to speed up the 10 minute average settlement time, but this would be antithetical to network decentralization by making it more difficult/costly to run a node).

Now let’s say you’ve come to terms with the security of the network and you firmly believe this asset will be an excellent store of value over time. You decide you want to buy some bitcoin and you’re going to invest a large sum of money into it. The network might be secure at a macro level, but you want to ensure the security of your own bitcoin. How do you protect your bitcoin from hacks, theft, loss, and other vulnerabilities?

This was one topic I really struggled with initially. It seemed to me like the barrier to entry (in terms of personal security) was too high. Securing my personal stake in some cryptographic monetary technology sounded super complicated. There’s a range of complexity when it comes to security, but there are a few simple steps that anybody can take to ensure their bitcoin is highly secure.

Why your bitcoin is secure on the blockchain

Bitcoin uses cryptographic hashing and digital signatures (the connection of private and public keys) to enable secure saving and spending of your bitcoin. Put simply, complex algorithms create public and private keys that allow you to received/store/send. The use of cryptography is important as it is a method to protect information (in this case, your private key) so that only you have access to it. The blockchain is transparent, so the transaction of buying bitcoin is broadcast to the network, but no personal information about the individuals making that transaction is shared. The verification process on the blockchain ensures that only you can spend your bitcoin, so long as you hold your own private key.

Public and private keys4 are essentially the way bitcoin is moved around on the blockchain. Your public and private key are tied together — the public key is used to received bitcoin and the private key is used to send it. Public and private keys are simply very large numbers that are recognizable by the blockchain.

Your private key is a randomly generated number you want to keep safe (think of it as an extremely complex password that can’t be guessed or hacked by even ultra sophisticated algorithms). The public key is generated off that private key so that you can receive bitcoin tied to that private key. It’s important to note that even though the public key is derived from the private key, there is no way for anyone to link your public to your private key. Ownership of your private key is essentially how you hold your own bitcoin. If you leave bitcoin on an exchange, they hold your private keys and therefore you personally do not own that bitcoin.

“When a bitcoin is spent to a public address, it is essentially locked in a safe, and in order to unlock the safe to spend the bitcoin, a valid signature must be produced by the corresponding private key (every public key and address has a unique private key). The owner of the private key produces a unique signature, without actually revealing the secret itself. The rest of the network can verify that the holder of the private key produced a valid signature, without actually knowing any details of the private key itself. Public and private key pairs are the foundation of bitcoin. And ultimately, private keys are what control access rights to the economic value of the network.” — Parker Lewis

Steps to secure your private keys

As I mentioned above, if you are having an exchange or a bank hold your private keys, then you are entrusting that they won’t be hacked, won’t suffer any liquidity issues, and won’t be subject to regulatory capture. To protect against this, you can hold your own key — but you need to do so securely. If someone is able to locate your private key, they now have the ability to spend your bitcoin.

Store your private key offline. This is referred to as ‘cold storage.’ There are a variety of hardware wallets that are fairly inexpensive you can buy to store your private keys. This ensures that your private key cannot be ‘hacked’ or taken from your computer in any way.

Store your hardware wallet somewhere secure, like a fireproof safe to prevent physical damage to your hardware wallet.

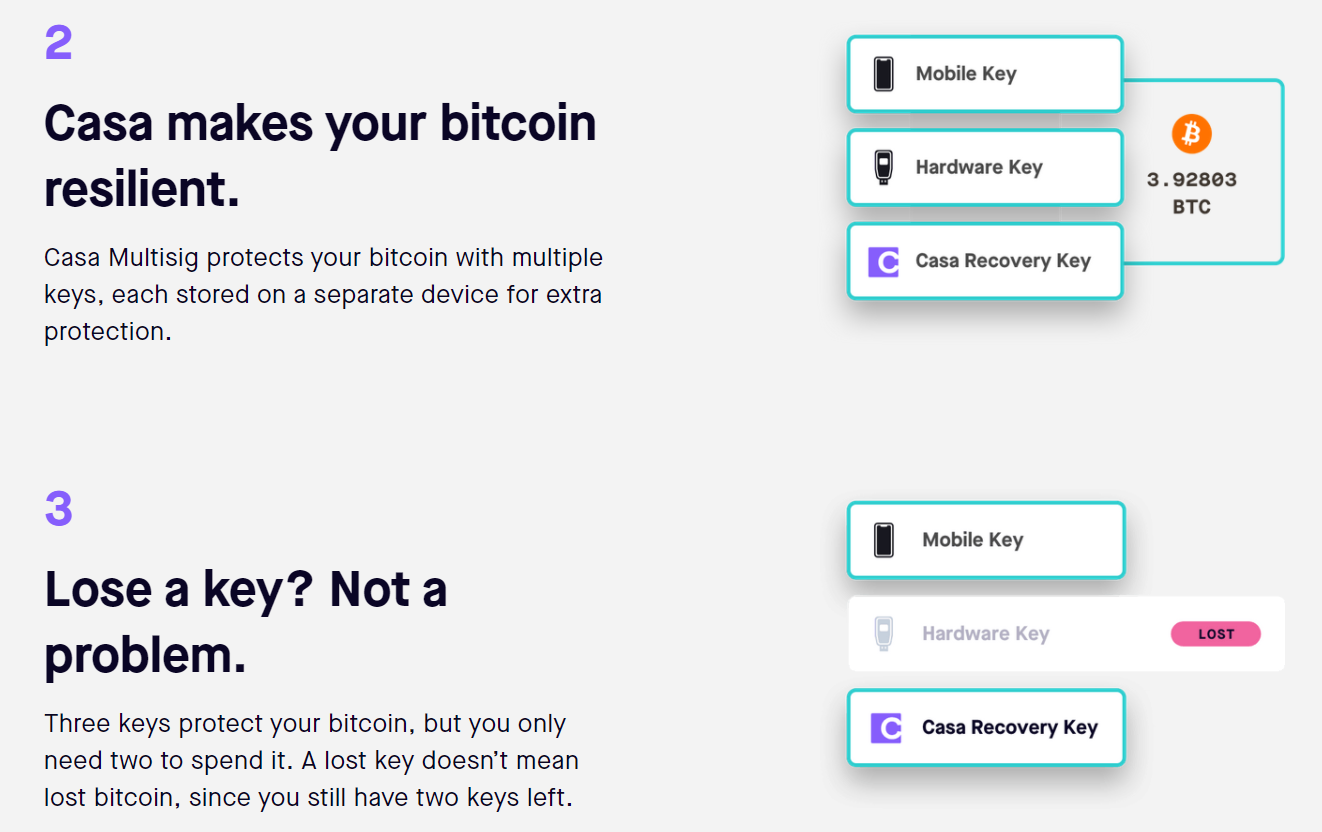

Use multi-sig (short for multiple signatures). Multi-sig sounded complicated to me at first, but it’s actually quite simple. With multi-sig, multiple keys are required to spend your bitcoin. So if your hardware wallet is stolen, no big deal — your bitcoin can’t be spent even if the thief has access to that one private key. You can set up multi-sig using a variety of combinations of keys. The below depiction is a simple way to envision how a set-up might look.

Some people are perfectly comfortable leaving their bitcoin on an exchange or solely trusting one single custodian to hold their private keys. If you have any concerns with that approach (I think you should), you can take all of the steps above with just a little bit of research and a small sum of money.

So the Bitcoin network is highly secure and you’ve now taken steps to secure your bitcoin savings by holding your own private keys via multi-sig. But you want to keep a small portion of bitcoin to spend on a regular basis. Won’t you have to wait 10 minutes for the transaction to settle when buying a cup of coffee or sending it to a friend? This is where the Lightning Network comes in.

Payments & Speed

I’ve talked about currency issuance and transaction settlements, as well as Bitcoin’s security. The final layer of a monetary network that I want to cover is payments. Payments and speed go hand in hand. Payments represent the layer of money that most impacts users on a daily basis, and speed is a critical element to a successful payments technology.

A false image has been painted by Bitcoin’s skeptics of people waiting in line at Starbucks for 10 minutes until their bitcoin transaction settles. In reality, people use bitcoin all over the world for day-to-day payments experiencing near-zero fees and settlement in milliseconds. The Lightning Network — a payments layer built on top of bitcoin — makes this all possible.

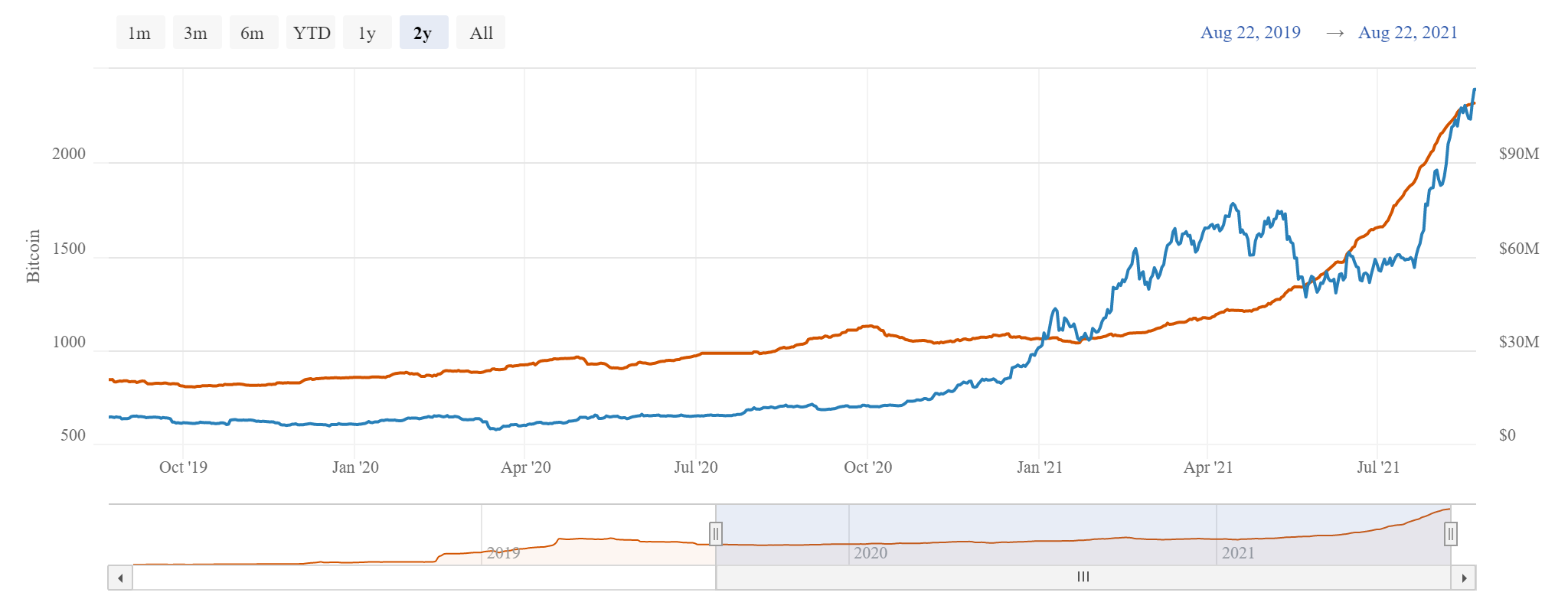

A primary (and justified) criticism of the Lightning Network has been a relatively low rate of adoption resulting in a lack of liquidity. As a new technology built on top of a new monetary network, I’m not sure why you’d expect anything else in the early days. But those early days are in the rearview now. The above graph illustrates how the Lightning Network’s capacity has exploded over the past few months, now sitting at nearly 2,300 BTC (over $100 million in USD value). In the above chart, the blue line represents Lightning Network capacity in terms of USD value and the red line represents capacity in terms of sum of BTC. It’s telling that despite the sharp decline in USD value of bitcoin in May of this year, Lightning Network capacity (in terms of BTC) continued to grow at a rapid pace.

This short video does a great job of very simply explaining how the Lightning Network works. There is a lot of more detailed and more technical content out there if you are looking to learn more, but I won’t be getting into the technical details in this article.

Simply put, the Lightning Network is a payments technology that uses bitcoin — similar to how Visa offers a payments technology using the U.S. Dollar (and other currencies). I mentioned earlier that comparing Visa to Bitcoin’s base layer (the layer optimized for security) was not a great comparison. A better comparison would be to pit Visa against the Lightning Network.

Visa handles about a couple thousand transactions per second (and they don’t settle for up to a few days). The Lightning Network can handle millions of transactions per second, and it provides instant settlement.

Visa charges around 1.5%-2.5% processing fees. Fees on the Lightning network are extremely low, as low as 1 satoshi (satoshis or “sats” are the smallest units of bitcoin), which would be less than a penny.

So using the Lightning Network is actually faster and cheaper than Visa, providing further evidence against the “bitcoin is too slow” argument. The Lightning Network certainly has a long way to go in terms of adoption to catch up to Visa and other major credit card networks, but it is a promising technology that is already helping scale Bitcoin beyond where many skeptics thought it would never reach.

My Take

When I first started learning about Bitcoin a thought that crossed my mind was, well it’ll probably just get hacked. I imagine a lot of people think that way when they try to envision what could go wrong with digital money. The more and more I learned about the network I realized just how strong it is. A truly open-source and decentralized monetary network is inherently more secure than a closed and centralized monetary network — there are simply fewer attack vectors.

And once I educated myself further about how our current money system works, I began to see through many skeptics’ comparisons. Comparing Bitcoin’s base layer to Visa is either misguided or disingenuous. This poor comparison makes it seem slow. In reality, Bitcoin is really, really fast.

Bitcoin trumps current and past moneys in terms of speed and security, not the other way around. As more and more people get over these hurdles, adoption will continue to spread, strengthening the network and further debunking the concerns that it can’t succeed as a medium of exchange.

“It doesn’t matter whether someone has one-tenth of a bitcoin or ten thousand bitcoin. Either and each are secured and validated by the same mechanism and by the same rules. Everyone has equal rights. Regardless of the economic value, each bitcoin (and bitcoin address) is treated identically within the bitcoin network. If a valid signature is produced, the transaction is valid and it will be added to the blockchain (if a transaction fee is paid). If an invalid signature is produced, the network will reject it as invalid. It does not matter how powerful or how weak any particular participant may be.” — Parker Lewis

Wrapping Up

And that wraps up the discussion around Bitcoin speed and security. Thanks so much for tuning in.

Remember to subscribe if you don't want to miss out on future newsletters. You can check out the Why We Bitcoin archive for previous posts and follow me on Twitter for more takes on all things Bitcoin.

Continue to scroll down if you’re interested in content that has helped me learn about this topic and for a brief preview of future topics.

3 Things to Read:

Unchained Capital: Bitcoin is Not Backed by Nothing by Parker Lewis

Coindesk: The Lightning Network is Going to Change How You Think About Bitcoin by Jeff Wilser

Binance Academy: A Beginner's Guide to Bitcoin's Lightning Network

3 Things to Listen to:

The Investor’s Podcast: Bitcoin Security and Self Custody with Nick Neuman

What Bitcoin Did: Introduction To Lightning with Christian Decker

Bitcoin Magazine Podcast: Onboarding the Masses to Lightning with Desiree Dickerson

Next time, I’ll cover the misconceptions that bitcoin is too expensive and too confusing. I remember thinking bitcoin was already too expensive at $5k (currently in north of $50k at the time of this writing) and I certainly was confused about what bitcoin was, how it worked, and why it was important when I first heard about it.

M2 and M3 money stock go on to further encompass things like savings accounts, bonds, and other liquid assets that are easily convertible into cash.

https://www.cnbc.com/2021/07/13/consumer-price-index-increases-5point4percent-in-june-vs-5percent-estimate.html

ACH transfers are unique to banks in the U.S.

This is an extremely simple primer on public and private keys https://getbitcoinclarity.com/blog/2020/05/16/what-is-a-bitcoin-private-key